- Kearney’s market study, European telecoms 2026: in need of a health boost, pins the region’s sectoral malaise on failure to leverage investment, caused by regional fragmentation.

- The gap in scale, consolidation, and market structure between Europe and the US is stark, with three-player markets consistently outperforming.

- Europe does not intrinsically lack infrastructure: the fundamental problems are insufficient returns on investment and weak capital efficiency, culminating in constrained reinvestment capacity.

- Network resilience is also now a vital sign of telco health, with Kearney advising strong pre-emptive action to counter growing threats and reputational danger.

- Kearney maps out seven interconnected action paths for transforming telco fortunes, spanning fibre commercialisation, AI-driven CVM, cost reduction, resilience, satellite, B2B ICT, and private capital — collectively pointing towards a virtuous cycle of scale, returns, and reinvestment.

- The B2B and ICT opportunity, valued at approximately $1.3trn and growing fast, remains underexploited, with telcos well positioned as sovereign digital partners if they can simplify and industrialise their delivery models.

- The vast investment gap to deliver a robust future may require external investment, with private equity offering a valuable source of patient capital in return for a clear and credible asset structure.

Where many consultancies may take the pulse of the sector when considering the state of the telecoms market, Kearney has gone one further and declared it has conducted a thorough check-up of the European scene with its recent report, European telecoms 2026: in need of a health boost.

The diagnosis, based on the consultancy’s European Telecom Health Index, suggests that while underlying fitness is still there, the symptoms of bigger, potentially serious issues are growing and the risk of further decline is rising.

After ranking 20 key European economies based on factors including operators’ financial performance, commercial credentials and technology capability, as well as the national business environment and customer perception, the detailed health check highlights treatments that Kearney considers can return the sector to wellness, with seven “action paths” tackling the gamut of digital infrastructure and customer engagement.

European telco frailty is not the result of a lack of digital infrastructure, stresses Kearney. The fundamental flaw is that the region has been building more than it has been monetising.

Failure to generate adequate investment returns and leverage capital efficiently has entrenched the malaise and vulnerability, including constraining capacity to reinvest in the capabilities and innovation required to recuperate.

The underlying problems cannot be tackled by tinkering or applying quick fixes, with the prescribed remedies collectively linked to driving revenue growth, enhancing efficiency and ROI, and improving resilience.

Central to creating an environment for industry revitalisation is fundamental change in the structure of the European telecoms market to enable greater realisation of the region’s potential for scale opportunities and benefits. Refreshed rules and an evolved outlook from national and regional policymakers will be critical.

Speaking to TelcoTitans, three of the key Kearney Partners behind the research — Christophe Firth, Christoph Neunkirchen, and Owen Tracey — explain how understanding and embracing the full potential of telecoms across the region can help return Europe to prominence as a global digital powerhouse, enabled by scaled players that are forward-looking, competitive, and equipped for sustained investment.

The scale of the challenge, and the challenge of scale

Operators in Europe are often quick to highlight the challenges they face when compared to the United States, with the latter’s regulatory and commercial environment deemed more amenable, and its business models more sustainable.

Kearney’s analysis supports the belief that there is a gulf between the geographies, with an average score on the European Telecom Health Index of 63 across the ten worst performing nations, compared to 73 for the US.

The population of the US is 340 million, while the European laggards are home to a comparable 354 million. The latter cohort represents nearly two-thirds of both population and GDP for the 20 countries scoped in Kearney’s study, but the subset’s real-world GDP of €15.5trn is far lower than the US’s approximate €29tn equivalent, underlining how competitiveness is being undermined and the ability to lead in innovation stifled.

Having also applied its Telecom Health Index methodology to the US, Kearney noted that the market has seen consolidation from four to three operators, which is a recurring feature of higher-performing markets (and a trend that has been no better than gradual within Europe). The US scores well on financial performance and technology deployment for its operators, which also have significantly larger subscriber bases (all in excess of 100 million).

While John Stankey, CEO of AT&T, recently took to the Mobile World Congress stage to praise “healthy” levels of intermodal competition, it is not simply a case of less competition and more relaxed regulation. US operators also share a rich home market with many of the world’s leading multinational corporations and can tap into an extended regional trading bloc. This provides ‘absolute scale’ opportunities and economies for US that currently have no comparable in Europe, which only has ‘minimum efficient scale’ at country level.

Europe is home to mobile groups with regional and global subscriber bases larger than the US players, such as Orange, Telefónica, and Vodafone, but Kearney considers these constructs to extract limited synergistic scale benefits due to country-level regulatory fragmentation and market restrictions. Deutsche Telekom is an outlier with transatlantic presence through control of T-Mobile US.

Kearney nonetheless sees opportunity for Europe to create circumstances that emulate the strengths of the US market, such as strategically targeted regulation and an approach to sovereignty that supports the bigger picture and not just national borders.

Beyond borders: engineering scale for a continental market

Owen Tracey proffers a thought experiment on enabling Europe to achieve some of the absolute scale from which the US benefits.

He posits that if Europe could embrace the idea that specific areas can become hubs of geographic specialised activity for the continent — “regional champions” akin to Silicon Valley as the US’ technology epicentre, New York as its financial capital, and Minnesota its medical leader — the entire continent could be lifted by the strength these clusters could generate.

Europe does have clusters, but these are constrained by regulatory complexity and a mindset of national rather than regional interest. This means investors bear a massive risk of deploying capital at no more than country level, and as a result often simply refrain.

Tracey’s thought experiment points to a more deliberate model of specialisation, in which hubs are embraced for cross-border sector leadership within a more integrated European market.

“ When you have that hub concentration and you have those cross-border data flows, that’s when you get meaningful investment. It also requires scale, international collaboration, and clear European standards, as well as the right regulatory environment. ”

Tracey.

This approach would demand a commitment to thinking and trusting beyond national boundaries, with cross-border data flows and an understanding of sovereignty as a capability that spans the region. For telecom operators, this would open up possibilities to draw national operations together on a multinational basis in pursuit of truly continental-scale benefits.

Three critical ailments

There are three dominant factors currently suppressing European telco sector health, according to Kearney:

-

Anaemic market concentration: in-market consolidation is shown to have clear impact in the index, bringing higher EBITDA margins and return on capital employed (ROCE). On the index’s key measures, three-player markets outperformed four-player counterparts in terms of financial performance (ten percentage points better), commercial ability, and business environment, although four-player markets showed marginally superior technology deployment and customer sentiment. Concentration is not just an in-country issue, with cross-border European consolidation considered essential to enabling the kind of scale that drives better operator returns and fosters further investment.

- Undervalued customers: in putting together the European telecoms 2026 report, Kearney conducted extensive consumer surveys in Europe and beyond, identifying correlation between telecom sector health and customer satisfaction. Countries that lead its Telecom Health Index with better-developed financial, commercial and technology foundations also see happier and more loyal customers willing to spend more on bundled services, with increased choice on availability of (revenue-generating) add-on services identified as a clear priority for customers. Conversely, the five markets lowest placed for sentiment were where churn was found to be high, services were considered less reliable and under-powered, and customer service was maligned. Customers were found to be well able to place this in context, too, with network quality emerging as a critical element of value perception and satisfaction, alongside low prices.

- Artificial intelligence stealing a march: AI is already deemed to be posing a risk to operators lagging in application of the technology for delivery of internal efficiency and accelerated service delivery. Conversely, reinvention as an AI-first service provider is viewed as a catalyst for transformation and an opportunity to break away from being perceived as a utility service provider. However, embracing AI is not about jumping on a bandwagon; adoption needs to be purpose-driven, focused on clear business goals linked to value creation, and delivering clear strategic benefits.

Kearney’s report encapsulated the regional malaise in seeing ROCE for European operators slump over a decade to 5.9% in 2023, from an already-low 6.7%. Also noted in the report is a 10% decline in mobile connectivity revenue in the 2016–2024 period (with fixed connectivity revenue down 3% over the same period). The impact of declining revenue is further exacerbated by inflation, with the EU consumer price index reporting a 31% rise over the same period.

AI looms over the telecom sector as both opportunity and existential risk. Kearney argues that operators that fail to harness AI for internal efficiency, customer value management, and speed of execution risk ceding ground permanently to hyperscalers and digital-natives, risking destiny as a utility provider rather than value-generating partner. The consultancy believes operators must stop treating AI as an IT project and start embracing it as a business transformation mandate. Regarding when a return will be seen on AI investments, Tracey is more circumspect but no less rousing, sharing a vignette from this year’s World Economic Forum, “the market is acting as if we can only measure returns when we’re finished investing and right now we’re in an arms race — we need to recalibrate for outcomes-driven investment ”. For European telcos, the risk is not merely commercial: without the scale and consolidated infrastructure to build or connect to AI-grade data centres, the region also risks falling further behind the US and China on the digital sovereignty agenda that the EU has made a strategic priority.

Heat is on in the Danger Zone

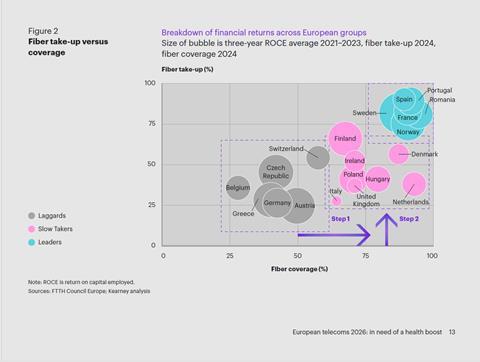

Kearney currently sees considerable risk for operators that are in what it classes as the ‘danger zone’ — an environment where infrastructure build is extensive, but adoption and monetisation are weak, undermining ROCE, future innovation, and the prospects for reinvestment.

The regional approach to fibre rollout provides a telling example of the perils of building digital infrastructure but not harnessing demand to monetise the investment.

Across the 20 countries examined, market ‘Leaders’ such as France, Spain, and Portugal are managing high deployment and high take-up, with next-generation connectivity now seen as standard in their markets and driving improved ROCE. Kearney’s survey data found that customers in these standout markets were significantly more satisfied across fixed and mobile services than for worst performers elsewhere, and more likely to buy multiple subscriptions. Another recurring characteristic of faster and more successful FTTH transitions has been coordinated national deployment strategies, avoiding the value-destructive overbuild or persistent black spots that can be features of markets where competition is unstructured.

At the other end of the scale, there are market ‘Laggards’ such as Belgium and all three DACH nations (Germany, Austria, and Switzerland) that have been slow to upgrade networks, with low deployment and low uptake. Superficially, this may not appear to be a problem, as EBITDA can be robust and ROCE even matching the level of Leaders at around 11%, based on functional existing infrastructure. However, sweating of legacy assets risks storing up future problems as offerings fall further behind and pressure builds to invest in catch-up, also suppressing demand for future digital services.

The greatest risk, however, is currently faced by ‘Slow Takers’. These are markets where modernised infrastructure is broadly in place but uptake has been underwhelming, putting pressure on financial performance and undermining development. Here, ROCE is weak at around 6%. There are some major markets in this uncomfortable position, with Italy, Poland, and the UK among those feeling the pinch, according to Christophe Firth.

“ If you look at the Danger Zone group, ROCE is just over half the level of the Leaders. So as a country, also as an operator, it’s a question of spending as little time as possible in that Danger Zone and getting up into the Leaders group once you’ve made the leap into full fibre. ”

Firth.

Hybrid fibre-coaxial cable operators are deemed to be in an awkward position regarding the Danger Zone, needing to consider not only ‘when’ but also ‘if’ at all to invest heavily in full fibre upgrades, with performance and monetisation uplift on DOCSIS infrastructure less clear than for ADSL with FTTC. The Netherlands’ VodafoneZiggo and Vodafone Germany have recently recommitted to HFC, while Virgin Media O2 in the UK is upgrading its HFC estate to full fibre.

Doctor’s orders for patient capital

Telcos manage a balancing act that is critical to sustained health, including juggling capex, paying dividends, and keeping current with infrastructure upgrades.

The trick to pulling this off in the long-term may be found in closer collaboration with strategically aligned private investors. “There’s a lot of patient and pragmatic capital out there: pension fund and private equity money looking for a home”, says Tracey.

The financial returns demanded on these longer-term bets are generally more modest, and operators are increasingly wise to the potential for finding new sources of funding in this field.

Tracey cites global investor KKR underpinning substantial amounts of Singtel’s data centre outlay, and AT&T bringing BlackRock into the GigaPower fibre joint venture as examples that are proving successful.

Pension funds are also notable institutional capital providers, such as Dutch pairings ABP/APG and PFZW/PGGM, which have respectively provided major backing to pan-European connectivity provider euNetworks and regional edge data centre specialist Penta Infra.

“ I think some operators have figured out this model that ‘we can be an owner-led but investor-funded telco’ and can still make decent returns. ”

Tracey.

The challenge, however, is having the right asset mix and structure in place.

When a telco entity comprises infrastructure and a network layer, topped with a service layer, valuing the assets becomes challenging with multiple valuation metrics in play. One possible approach is to simplify the asset mix to InfraCo, NetCo and ServCo components, making the presentation and maths clearer.

With infrastructure, expectations for returns can be measured in decades, while NetCo investment is more likely to be considered on a five-to-seven year cycle. For a ServCo, the metrics become more liquid, with almost annual reviews the norm, adding considerable complexity.

By not breaking out these different assets, telcos may be undervalued with a “conglomerate discount”, according to Tracey. “Unless you can break them out cleanly and show how to measure and value the assets, investors may be inclined to think you’re hiding or cross-subsidising something”, he further warns.

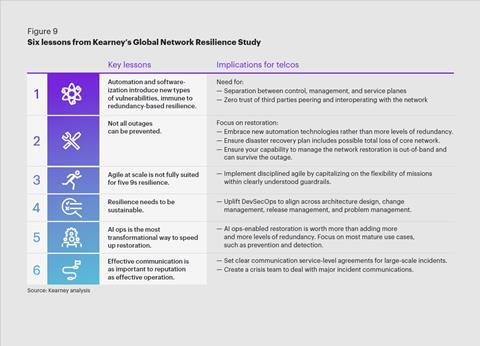

Resilience: from technical afterthought to boardroom priority

Future health for telcos will also be dependent on network resilience.

For telcos, this is now becoming a CEO-level priority, and Kearney’s Firth sees its importance at national and regional levels only increasing due to the substantial and growing level of risk from both malicious and non-malicious sources that can cause network outages. “It’s not a technical topic anymore,” he notes, “it’s a highly operating model-strategic topic”.

Resilience audits are set to become the norm, with Firth seeing the UK as, if not leading the way, certainly asking the right questions on how to ensure future reliability and stability. A standout is Australia, where the reaction to a major outage in 2023 led to creation of a National Telecom Resilience Centre at the University of Technology Sydney, a world-first institution dedicated to assessing and improving infrastructure resilience.

The subject of resilience goes beyond telco infrastructure, with Firth underlining the importance of working across sectors as telecoms network, smart electricity grid, and data centre are interconnected and increasingly interdependent. This is an issue, he believes, that will become a priority not only for operators but for national governments, regulators, and the European Union.

As a consultancy, Kearney sees the matter of resilience as central to the development of digital infrastructure. It has responded to the current parlous environment with specialist advisory and hands-on capability that includes an advisory panel of former C-level telecoms executives and a dedicated technology centre of excellence. These deep technical skillsets support work with operators to address threats and vulnerabilities, including providing direct oversight and insight.

Firth pointed to expanding interplay between telecoms and energy, another established critical infrastructure segment, including around power backup and resilience. At a strategy presentation in February, InfraCo Cellnex highlighted grid-integrated backup as an area being pursued in Spain, following the nation’s 2025 blackout. The infrastructure provider also noted that extreme storms had recently knocked out 60 mobile tower sites in Portugal, which was around the same number as usually lost in a year across its overall twenty-times’ larger entire European footprint.

Honey pots and on-ramps: the digital infra opportunity

Digital infrastructure needs to be seen holistically, with fibre, data centres, AI, and satellite connectivity contributing to a broader ecosystem that supports resilient operators, sustainable returns, and continued innovation.

The expansion of low-Earth orbit (LEO) satellite constellations, for example, has quickly expanded the role of non-terrestrial connectivity. However, notable current players such as Amazon Leo, AST SpaceMobile and Starlink are again based in the US. The continent does have a well-developed satellite sector with players in the LEO segment, such as Eutelsat’s OneWeb and Spain’s Sateliot, and it will be essential to ensure capability and sovereignty are protected as the importance of satcoms grows.

For telecom operators, Kearney advises leaning into this expansion of digital infrastructure to work collaboratively with non-terrestrial network providers and European authorities to leverage the opportunity to create value and generate revenue, and ultimately reinforce their customer relationships.

Tracey also considers that another expanding part of the European sovereign digital landscape, data centre providers, are building “a giant sticky pot of honey”. And for businesses to reach this treasure, they need to go through telcos.

“Just on connectivity, there are multiple needs”, he says, “there’s local connectivity, backbone, secure cloud edge”. And the telco role goes even deeper at the data centre itself, where there is need for a switching fabric that can orchestrate across different cloud platforms.

“ It’s all telco: the sovereign data centre sector could quickly expand an already existing market for telco services. Operators don’t need to compete with data centre players; they might be better served in putting that investment and effort into building better on-ramps and connectivity to sovereign-hosted workloads. ”

Tracey.

As Kearney’s strategies for European recovery weave together, investing across the board on digital infrastructure is seen as driving an essentially perpetual growth opportunity.

Christoph Neunkirchen resurfaces the importance of scale in this context, with regional sovereignty kickstarting the process, and guiding that operators, customers and nations can all benefit. The alternative of sector stasis risks decline.

As an example, Neunkirchen notes there were still 90 mobile network operators in Western Europe in 2025 — just two fewer than fifteen years earlier — while MVNOs continue to proliferate. This fragmentation has led to an environment where focusing on return on investment has become hugely challenging, underlining the need for rational consolidation and new approaches.

“ Europe’s problem is not a lack of infrastructure, it is a lack of sustainable returns on that infrastructure. Telecom needs to develop a virtuous cycle of scale, returns, and reinvestment, or face a downward spiral. Infrastructure without returns is not an asset, it is a liability. ”

Neunkirchen.

Kearney’s prescription: seven paths to European telecoms recovery

Kearney outlines seven “action paths” that it considers will help lead European telcos to recovery, embracing structural change and a rethink in operator mindset.

- Jumpstarting fibre commercialisation — as noted above, telcos can benefit significantly from ensuring that not only is their infrastructure modernised, but that it is widely adopted among the customer base, with returns seen to improve and customer satisfaction boosted in markets with significant fibre bases.

- Adopting a new B2B ICT model for growth — enterprise services have long been a Holy Grail for operators seeking new revenue streams, although many attempts have proven complicated and unprofitable. Kearney argues that telcos can either retreat to their core businesses, or reset their B2B ICT strategy to leverage strengths in delivering sovereign services that are increasingly in demand and build on areas where network differentiation provides an edge. Kearney’s report urges operators to take the opportunity presented by AI disruption to break with previous attempts to tag ICT onto traditional models, and adopt a new approach with distinct leadership and incentives, and simplified and industrialised delivery models. The rewards are worth it, with the consultancy pointing to an addressable regional market valued at $1.3trn in 2025 and growing at 10% annually, as well as substantial pent-up demand among mid-market enterprises and public sector entities seeking trusted local partners. This strategy refocus is already showing success for players like KPN, Swisscom, and Vodafone.

- AI-powered customer value enhancements — Kearney considers that greater attention needs to be paid to Customer Value Management, and that AI provides a way for operators to adopt data-driven approaches that can improve margins and customer experience, with lessons to be learned from experts such as Netflix. Effective CVM is said to be able to “lift direct margins by 2.5 percentage points, increase ARPU by up to 15%, and reduce churn by as much as 10%–15%”.

- “Advanced” cost reduction — the capital intensity of the telco model needs a rethink, and Kearney sees strategically guided adoption of automation, ‘platformisation’, cloudification, and smart governance of spending as presenting an opportunity to break away from the drain of tech debt and legacy processes. This is a change, they believe, that can be achieved with a new mindset, and a dose of organisational courage.

- A stronger digital backbone through network resilience — telecoms environments are becoming more complex and no less critical within everyone’s lives. With outages having serious consequences operationally and reputationally, Kearney is pushing European operators to protect their position with a clear-eyed review of current status, introduction of goals for improvement, and action on implementing tools supporting greater robustness.

- Satellite communications strategy that supports the sector — non-terrestrial network services are increasingly common and operators need to embrace their rapidly evolving capabilities to complement their own strengths. With customer and regulatory expectations rising on ubiquitous connectivity, operators must act to ensure satellite connectivity is used to enhance rather than weaken existing customer relationships, without becoming overly-reliant on non-European partners.

-

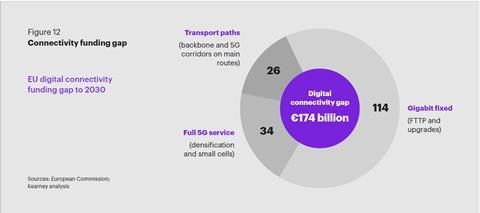

Private equity cash injections to boost digital infra growth — the gap between aspirational connectivity targets for Europe and the reality of investment earmarked over the next five years is put at €174bn. Kearney sees strategically-targeted partnerships as a way for operators to fund their own ambitions as well as those of the European Union, without surrendering control or value of assets. As Tracey explains above, this will demand a clear understanding of the private finance mindset.

The full European telecoms 2026: in need of a health boost report dives deeper into the steps that telcos need to take to progress on these paths, and illustrates benefits the consultants see flowing from making a strategic shift. Kearney is continuing to evolve its research, with granular examination of sector performance around the world set to flow into a global Telecom Health Index.

Topics

- AI/GenAI/ML (artificial intelligence, agentic, machine learning)

- AT&T

- Australia

- Austria

- BlackRock

- Capex (capital investment)

- Cellnex

- China

- Christoph Neunkirchen

- Christophe Firth

- Customer service

- Customer/User experience (CX/UX)

- Data centre

- Enterprise (B2B)

- Europe

- European Union (EU, EC, EP)

- Fibre (FTTC/FTTP)

- Financial & Performance

- France

- Germany

- Infrastructure

- Italy

- John Stankey

- Kearney

- KKR

- KPN

- Mergers and Acquisitions (M&A)

- MWC (GSMA Mobile World Congress)

- Netflix

- Network & Infrastructure

- Optus

- People

- Poland

- Portugal

- Public Affairs

- Satellite

- Singtel

- Spain

- Strategy & Change

- Swisscom

- Switzerland

- United Kingdom (UK)

- United States (USA)

- Venturing & Investments

- Vodafone Group

- Wholesale